Yes, profits from forex trading are taxable in Australia. The Australian Taxation Office (ATO) requires you to report all gains, but how they are taxed depends on whether you are classified as a hobbyist, an investor, or a business trader. Your classification impacts your tax rate, the deductions you can claim, and how you report your income. Finding a regulated forex broker is the first step, but understanding your tax obligations is crucial for long-term success. This guide will cover everything you need to know about Forex Tax in Australia for the 2025 financial year.

Key Takeaways

- Tax Is Mandatory: All profits from forex trading are considered assessable income by the ATO and must be reported.

- Classification is Crucial: How you’re taxed—as a business on income or an investor on capital gains—depends on factors like your trading frequency, volume, and intent. This is the single most important factor determining your tax outcome.

- Two Main Tax Treatments: Profits can be treated as ordinary income (taxed at your marginal rate) or as a Capital Gains Tax (CGT) event. Investors holding currency pairs for over 12 months may be eligible for a 50% CGT discount.

- Record-Keeping is Non-Negotiable: Under new ASIC and ATO scrutiny, meticulous record-keeping of every trade, including dates, currency pairs, amounts, and broker statements, is essential to substantiate your tax position and deductions.

- Losses Can Be Useful: Trading losses can be used to offset capital gains (for investors) or other income (for business traders), but strict rules apply.

- Reporting is at Trade Closure: Tax obligations are triggered when you close a position, not when you withdraw funds from your broker account.

Disclaimer: The information provided in this article is for general informational purposes only and does not constitute financial or tax advice. The rules surrounding Forex Tax in Australia are complex and subject to change. You should consult with a qualified and registered tax agent or financial advisor to understand your personal circumstances and ensure compliance with the Australian Taxation Office (ATO) regulations. The examples provided are illustrative and may not apply to your specific situation.

Do You Owe Taxes on Forex Trading?

One of the first questions aspiring traders ask is whether their forex profits are subject to tax. The answer is an unequivocal yes. The ATO views profits derived from the buying and selling of foreign currency contracts as assessable income. There is no tax-free threshold specific to trading; any profit you make must be declared. The critical question isn’t if you pay tax, but how your activities are classified and taxed.

The ATO doesn’t have a separate set of laws just for forex; instead, it applies existing tax principles. Your trading activities will generally fall into one of three categories, each with distinct tax implications.

- Trading as a Hobby: This is extremely rare for forex trading and difficult to prove. If you were merely dabbling with no real intention of making a profit (e.g., buying a small amount of foreign currency for a trip and making a tiny gain), your profits might not be taxable, but neither are your losses deductible. Given the leveraged nature and speculative intent of forex, the ATO will almost never consider it a hobby.

- Trading as an Investor (Speculator): This is the most common classification for individuals who trade part-time. You are making speculative investments with the intention of profiting from currency movements. Your profits are treated as capital gains and are subject to Capital Gains Tax (CGT). This can be advantageous, especially if you qualify for the 50% CGT discount.

- Trading as a Business: If you trade frequently, systematically, and with a significant amount of capital and sophistication, the ATO may classify you as carrying on a business of forex trading. In this case, your profits are treated as ordinary business income and taxed at your marginal income tax rate. While this means no CGT discount, it opens the door to a wider range of business expense deductions. Understanding these differences is fundamental to managing your Forex Tax in Australia.

Latest 2025 ATO & ASIC Tax Rules

The regulatory landscape for financial markets is constantly evolving, and 2025 is no exception. While the core principles of Forex Tax in Australia remain consistent, enhanced oversight from both the Australian Taxation Office (ATO) and the Australian Securities and Investments Commission (ASIC) has introduced new compliance pressures for traders. From my experience, staying ahead of these changes is key to avoiding trouble.

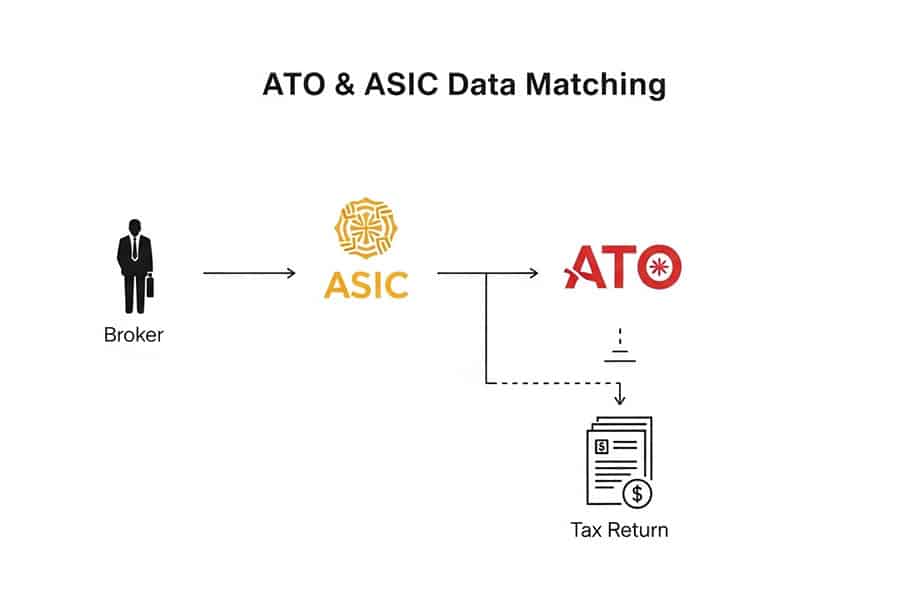

Compared to 2024, the primary shift for the 2025 financial year is a heightened focus on data transparency and record-keeping. Prompted by new ASIC derivative transaction reporting rules, the ATO now has unprecedented access to trading data from regulated brokers. This means discrepancies between your broker’s data and your tax return are easier than ever to spot.

Key Changes and Focus Areas for 2025:

- Enhanced Transaction Reporting: ASIC’s updated rules require brokers to provide more granular reports on derivative transactions, including CFDs on forex. The ATO is leveraging this data to cross-reference with taxpayer declarations. Any undeclared profit is a massive red flag.

- Stricter Record-Keeping Scrutiny: While keeping good records has always been important, it’s now a critical defence. The ATO expects traders to maintain comprehensive logs that justify their classification as an investor or a business. Simply relying on an annual broker statement is no longer sufficient if you are claiming business status.

- ATO Data Matching Programs: The ATO’s data matching capabilities now extend more deeply into financial institutions, including third-party payment processors and international brokers. They are actively looking for funds flowing to and from trading platforms.

For non-resident traders, the impact of these changes is also significant. If you are trading through an Australian-regulated broker, your data is still being reported. While Australian tax law may not apply to you depending on your residency status and any double-tax agreements, the increased transparency means your home country’s tax authority may have an easier time obtaining your trading information. Properly understanding the forex trading tax rules Australia has in place is more important than ever.

Income or Capital Gain: How to Classify

The cornerstone of managing your Forex Tax in Australia is correctly classifying your trading profits as either ordinary income or a capital gain. This single decision dictates your tax rate, the deductions you can claim, and how losses are treated. The ATO does not provide a simple, black-and-white definition; instead, it uses a set of principles often called the ‘badges of business’ to determine if you are a business trader or an investor/speculator.

Getting this classification wrong can lead to audits, back-taxes, and penalties. As a trader, I’ve found it’s best to assess your activities against these criteria honestly at the start of each financial year. Let’s break down the factors the ATO considers in its trader vs. investor test.

| Factor | Indicates a Business (Trader) | Indicates an Investment (Investor/Speculator) |

|---|---|---|

| Frequency & Volume | High volume of trades, often daily or weekly. Repetitive and systematic transactions. | Infrequent, irregular trades. May hold positions for weeks, months, or longer. |

| Intent | Primary intention is to generate regular income for a livelihood through a commercial operation. | Intention is to generate a profit from an asset’s appreciation over time, often alongside other primary income sources. |

| Business Structure | Operating through a registered business structure (e.g., ABN, company, trust), maintaining a business plan, and having separate bank accounts. | Trading in a personal capacity without a formal business structure. |

| Capital Employed | Significant capital invested, often leveraged, which is turned over regularly for profit. Capital is treated like ‘trading stock’. | Capital is invested on an ad-hoc basis. The amount may be smaller and not a primary source of funds. |

| Sophistication & Skill | Using sophisticated tools (e.g., paid software, EAs), having a detailed trading strategy, dedicating significant time to research and execution. | Relying on basic broker platforms, news, or general market sentiment. Trading is less organised. |

How to Get a Private ATO Ruling

If you are genuinely unsure about your classification, you can apply to the ATO for a private ruling. This is a formal, written clarification of how the tax law applies to your specific circumstances. While the process can be time-consuming, it provides you with certainty and is binding on the ATO, protecting you from future penalties if you have provided all the correct information. For traders with significant capital or complex situations, this can be a worthwhile step in correctly managing their Forex Tax in Australia.

Which Tax Rate Applies to Your Profits?

Once you’ve determined your classification, calculating your potential tax bill becomes much clearer. The tax treatment for a business trader and an investor are fundamentally different, directly impacting your final after-tax return. This is a crucial element of the forex trading tax rules Australia has established.

Ordinary Income for Business Traders

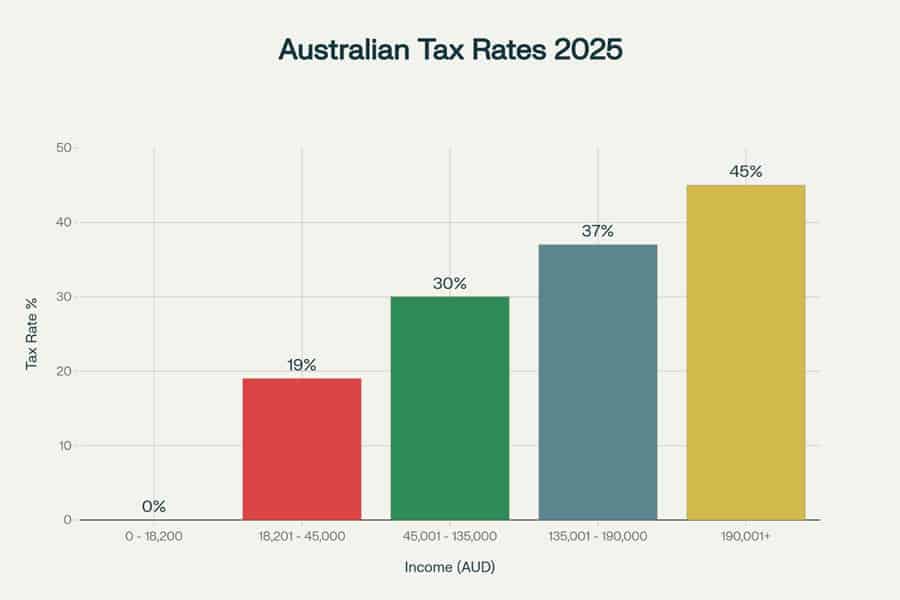

If you meet the criteria for carrying on a business of forex trading, your net profits are treated as assessable income. This means your total profit for the financial year (gains minus losses and deductible expenses) is added to your other income (like a salary from a job) and taxed at your individual marginal tax rate. For the 2024-2025 financial year, these rates are:

- $0 – $18,200: 0%

- $18,201 – $45,000: 19%

- $45,001 – $120,000: 30%

- $120,001 – $180,000: 37%

- $180,001+: 45%

Note: These rates do not include the Medicare levy of 2%.

Capital Gains Tax (CGT) for Investors

If you are classified as an investor or speculator, your profits and losses fall under the Capital Gains Tax (CGT) regime. Each time you close a forex contract, a CGT event occurs. Your capital gain for a trade is the proceeds from closing the position minus its cost base. Your net capital gain for the year is your total capital gains minus your total capital losses.

The most significant advantage for investors is the 50% CGT discount. If you hold a forex contract (asset) for more than 12 months before closing the position, you can reduce the taxable capital gain by 50%. The remaining 50% is then added to your assessable income and taxed at your marginal rate.

Example Tax Calculations

Let’s illustrate the difference with two scenarios. Assume both traders have a separate salary of $80,000 and made a net profit of $30,000 from trading.

Scenario 1: Chloe, the Business Day Trader

- Trading Profit: $30,000

- Other Income: $80,000

- Total Assessable Income: $30,000 + $80,000 = $110,000

- The $30,000 profit is taxed at her marginal rate of 30% (plus Medicare levy).

- Tax on Trading Profit: $30,000 * 30% = $9,000 (approx., excluding levy)

Scenario 2: David, the Part-Time Investor

- Trading Profit: $30,000 (from positions held over 12 months)

- He is eligible for the 50% CGT discount: $30,000 * 50% = $15,000 discount.

- Taxable Capital Gain: $30,000 – $15,000 = $15,000

- Other Income: $80,000

- Total Assessable Income: $15,000 + $80,000 = $95,000

- The taxable portion of his gain is taxed at his 30% marginal rate.

- Tax on Trading Profit: $15,000 * 30% = $4,500 (approx., excluding levy)

As you can see, the correct classification can halve the tax liability on the same amount of profit. This highlights why understanding the nuances of Forex Tax in Australia is so important for your bottom line.

Essential Records and Tax Forms

Meticulous record-keeping is not just good practice; it’s a legal requirement and your best defense against an ATO audit. With ASIC and the ATO sharing more data than ever, your records must be impeccable. You need to know exactly how to report forex trading for tax Australia requires, and that starts with your documentation.

From my own journey, the moment I started treating my record-keeping like a core business function, tax time became infinitely less stressful. You should document transactions as they happen, not try to reconstruct them months later.

Mandatory Records for All Forex Traders

Regardless of whether you are a business or an investor, the ATO expects you to keep detailed records for at least five years. These include:

- Detailed Trade Logs: This is more than just your broker statement. A spreadsheet is ideal. For every single trade, you must record:

- Date and time the position was opened

- Date and time the position was closed

- Currency pair traded (e.g., AUD/USD)

- Direction of the trade (Buy/Long or Sell/Short)

- Opening and closing prices

- Size of the position (e.g., lots, units)

- Gross profit or loss in the currency of the trade

- Gross profit or loss converted to Australian Dollars (AUD)

- Any commissions or financing charges (swaps) paid

- Broker Statements: Download and save all monthly and annual statements from your broker. These serve as primary evidence to corroborate your trade log.

- Bank and Payment Processor Statements: Keep records of all fund transfers to and from your trading account. The ATO uses this data to track money flow.

- Expense Receipts: If you are operating as a business, you must keep receipts for all claimed deductions, such as software subscriptions, educational courses, or computer equipment.

A crucial point many new traders miss is about timing. A tax event is triggered when you close a trade, realising a gain or loss. It is not triggered when you withdraw money from your broker account. If you make $20,000 in profit within a financial year but leave it all in your trading account, that $20,000 is still assessable for that year.

Which ATO Forms to Use

When it comes time to lodge your tax return, you’ll report your forex activities in different sections depending on your classification:

- For Investors (Capital Gains): You will complete the ‘Capital gains or losses’ section of your individual tax return (myTax for most people). You’ll need to report your total current year capital gains and losses. If you’re claiming the 50% discount, you calculate it here.

- For Business Traders: You will complete the ‘Business income or loss’ section. If you have an ABN, you will likely fill out the ‘Business and professional items’ schedule. Here you report your gross earnings as business income and then list your deductions to arrive at your net profit or loss.

Knowing how to report forex trading for tax Australia-style means using the right forms and having the records to back up every number you enter.

Deductions & Losses: Minimize Your Tax Bill

Effectively managing your tax bill isn’t just about paying what you owe; it’s also about legally minimising it by claiming all eligible deductions and correctly applying losses. The rules for this differ significantly between business traders and investors, another reason why your classification is so vital for your Forex Tax in Australia strategy.

Deductible Expenses for Business Traders

If you are carrying on a business of forex trading, you can deduct any expense that is directly related to earning your trading income. This is a major advantage of the business classification. Common deductions include:

- Trading Software and Platforms: Subscriptions to charting software (e.g., TradingView), analytical tools, or Virtual Private Servers (VPS) for running expert advisors.

- Data Feeds: Costs for premium news or data services.

- Education: Expenses for courses, seminars, or books directly related to improving your trading skills. Self-improvement must be linked to your current income-earning activities.

- Home Office Expenses: If you have a dedicated area for trading, you can claim a portion of your home running costs (electricity, internet) and depreciation on office furniture. The ATO has specific rules for calculating this.

- Computer and Office Equipment: The depreciation of computers, monitors, and other hardware used for trading.

- Accounting and Tax Agent Fees: The cost of professional advice for managing your trading tax affairs is deductible.

- Bank Charges and Interest: Bank fees on your trading account and interest on money borrowed to fund your trading activities may be deductible.

Using Trading Losses to Your Advantage

Losses are an inevitable part of trading, and the tax system provides ways to use them to your benefit.

- For Investors (Capital Losses): A capital loss from forex trading can only be used to offset capital gains. You must first apply it against any capital gains in the same income year. If you still have leftover capital losses, you cannot deduct them from your other income (like your salary). Instead, you must carry them forward to future income years to offset future capital gains.

- For Business Traders (Business Losses): If your deductible expenses exceed your trading income, you have a business loss. Under the ‘non-commercial loss’ rules, you may be able to offset this loss against your other income (e.g., salary) in the same year, potentially resulting in a significant tax refund. To do this, you generally need to satisfy one of four tests, such as having assessable income from the business of at least $20,000. If you don’t meet these tests, the loss is carried forward to be offset against future profits from that same business.

The tax treatment of algorithmic or automated trading generally follows the same principles. If it’s run with the sophistication, frequency, and intent of a business, it will be treated as such. Understanding these rules is key to a robust approach to Forex Tax in Australia.

Common Mistakes: How to Avoid ATO Penalties

Navigating the complexities of Forex Tax in Australia can be tricky, and mistakes can be costly. With the ATO’s enhanced data-matching capabilities, the chances of errors going unnoticed are lower than ever. From my experience observing other traders and consulting with tax professionals, most issues stem from a few common pitfalls.

The best way to avoid penalties is to be proactive and diligent. Think of your tax compliance as part of your trading strategy—managing risk. The new ASIC transparency rules mean your broker is already reporting on you; your job is to ensure your story matches theirs.

Typical Audit Triggers and How to Avoid Them

- Misclassifying Your Activities: Claiming to be a business trader to deduct expenses without meeting the ‘badges of business’ criteria is a major red flag. Avoid it by: Honestly assessing your trading patterns against the ATO’s guidelines. If you’re a part-time investor, embrace it and aim for the CGT discount rather than claiming deductions you’re not entitled to.

- Poor or Non-Existent Records: This is the easiest way to lose a dispute with the ATO. If you cannot substantiate your reported income, losses, or deductions, they will likely be denied. Avoid it by: Implementing a rigorous record-keeping system from day one. Use a spreadsheet or dedicated software to log every trade and save all broker and bank statements.

- Forgetting to Declare Income: Some traders mistakenly believe that if they don’t withdraw profits from their offshore broker, it isn’t taxable in Australia. This is false. As an Australian resident for tax purposes, you are taxed on your worldwide income. Avoid it by: Reporting all realised gains at the end of the financial year, regardless of where the funds are held.

- Incorrectly Calculating Capital Gains: Errors in calculating the cost base of a trade or incorrectly applying the 50% CGT discount (e.g., applying it to assets held for less than 12 months) are common. The australian taxation office forex gains rules require precise calculations. Avoid it by: Keeping a detailed log with dates to accurately determine the holding period of each contract and carefully calculating your net capital gain before applying any discounts.

Best practice is simple: be honest, be organised, and if in doubt, seek professional advice. The cost of a tax agent is a small price to pay for peace of mind and is often tax-deductible itself. A proactive approach to your Forex Tax in Australia is the best way to stay off the ATO’s radar.

Expert Tips for Traders: Save on Taxes

Beyond simply complying with the law, strategic planning can help you maximize your after-tax returns. A smart approach to Forex Tax in Australia can be just as important as a smart trading strategy. Here are some tips I’ve picked up over the years.

When to Consider Professional Advice

While you can lodge your own tax return, seeking professional advice from a tax agent specializing in trader taxation is often a wise investment. Consider hiring an expert if:

- Your trading profits are substantial.

- You are unsure whether you are a business or an investor.

- You want to set up a more complex trading structure, like a company or trust.

- You have significant capital losses you want to utilize correctly.

Strategic Planning for Better After-Tax Returns

- Plan Your Holding Periods: If you are an investor, be mindful of the 12-month holding period for the CGT discount. If a trade is profitable and approaching the 12-month mark, it might be worth holding on a little longer to qualify for the 50% tax reduction.

- Time Your Loss Realisation: If you have realised significant capital gains during the year, you might consider closing some losing positions before June 30th to generate capital losses that can offset those gains, thereby reducing your tax bill for the current year.

- Maintain a ‘Contemporaneous’ Diary: This is an expert tip. Alongside your trade log, keep a simple diary noting why you entered a trade, your strategy, and the time you spend on research. This can be invaluable evidence to support a business classification if questioned by the ATO.

The ultimate strategy for a stress-free tax season is discipline in record-keeping. Use software, use a spreadsheet, use anything—but use it consistently. Log every trade, every deposit, every expense. When June rolls around, you’ll thank yourself. Mastering the forex trading tax rules Australia imposes is a marathon, not a sprint, and good habits are your best friend.

Latest ATO Resources & Further Help

For the most definitive and up-to-date information, always refer to the official source. The Australian Taxation Office provides a wealth of guides and tools. Navigating the complex world of Forex Tax in Australia is easier with the right resources.

- ATO Website – Foreign exchange gains and losses: The primary ATO page covering the general principles.

- ATO Community Forums: A place to ask questions and see answers provided by ATO officials and the community. Many forex-related queries have been answered here.

- ATO Private Rulings: Information on how to apply for a binding private ruling on your trading status.

- Moneysmart.gov.au: An ASIC-run website with general guidance and warnings about forex trading.

Additionally, engaging with online trading communities and forums can provide practical insights, but always verify tax-specific information with a qualified professional or the ATO itself.

Trade with an Edge at Opofinance

As an ASIC-regulated broker, Opofinance provides a secure and feature-rich environment for Australian traders. Gain access to a suite of powerful tools designed to enhance your trading strategy:

- Advanced Trading Platforms: Choose from industry-leading platforms including MT4, MT5, cTrader, and the intuitive OpoTrade app.

- Innovative AI Tools: Leverage the AI Market Analyzer, get guidance from the AI Coach, and receive instant help from AI Support.

- Flexible Trading Options: Explore Social Trading to follow experts or test your skills with Prop Trading.

- Secure & Convenient Transactions: Enjoy peace of mind with safe deposits and withdrawals, including crypto payments with zero fees.

Elevate your trading experience with Opofinance today.

Conclusion

Successfully navigating Forex Tax in Australia is a critical component of being a profitable trader. While the rules can seem daunting, they boil down to a few key principles: all profits are taxable, your classification as a business or investor is paramount, and meticulous records are non-negotiable. By understanding the forex trading tax rules Australia sets out, planning your trades strategically, and seeking professional help when needed, you can ensure you meet your obligations confidently and focus on what you do best: trading the markets.

How does the ATO handle tax on forex CFDs?

While helpful as a summary, a broker’s report is often not sufficient on its own, especially if you’re claiming business status. The ATO expects you to maintain your own detailed, contemporaneous records to substantiate all figures in your tax return.

Is my broker’s annual tax report enough for the ATO?

While helpful as a summary, a broker’s report is often not sufficient on its own, especially if you’re claiming business status. The ATO expects you to maintain your own detailed, contemporaneous records to substantiate all figures in your tax return.

Can I prepay tax to avoid a large bill at tax time?

Yes. If you anticipate a significant tax liability from your trading, you can voluntarily enter the Pay As You Go (PAYG) instalment system. This allows you to make regular prepayments throughout the year, smoothing out your cash flow and avoiding a single large bill.

How do I calculate AUD value for many small trades?

The ATO allows for a practical approach. You can either convert each transaction at the time it occurs or use an average exchange rate over a reasonable period (e.g., daily or monthly). Consistency is key. The ATO publishes official average rates you can use.

What if I made a loss but don’t qualify as a business?

If you’re an investor and you have a net capital loss for the year, you cannot deduct it from other income. You must carry the loss forward indefinitely to offset against future capital gains from any source, not just forex trading.

Do I pay tax if trading on offshore platforms?

Yes. If you are an Australian resident for tax purposes, you are taxed on your worldwide income. It does not matter if your broker is located in Australia, Cyprus, or the Cayman Islands. Any realised profit must be declared to the ATO. The ATO’s data-sharing agreements with other countries are making it easier to track funds held offshore.

Is GST charged on forex trades?

No, Goods and Services Tax (GST) is generally not charged on forex trading for retail traders. Financial supplies, such as derivatives and foreign currency contracts, are typically input-taxed, meaning you don’t charge GST on your gains, and you generally can’t claim GST credits on your expenses.

How are forex losses handled?

It depends on your classification. For an investor, capital losses from forex can only be used to reduce capital gains, either in the current year or carried forward to future years. For a business trader, losses can potentially be offset against other income (like a salary) in the same year, subject to non-commercial loss rules.

What if I am a non-resident?

Non-residents are generally only taxed on their Australian-sourced income. Profits from forex trading conducted by a non-resident are often not considered Australian-sourced income and may not be subject to Australian tax. However, the rules are complex and depend on your specific circumstances and any applicable tax treaties. Professional advice is highly recommended.

Can I get a CGT discount?

Yes, but only if you are classified as an investor (not a business) and you have held the specific forex contract for more than 12 months before closing the position. If you meet these conditions, you can reduce the taxable capital gain by 50%.