Do You Pay Tax on Forex Trading in Canada? Yes, absolutely. Any profits you make from forex trading in Canada are taxable. The Canada Revenue Agency (CRA) requires you to report all earnings. However, how you’re taxed depends entirely on how the CRA classifies your trading activity. Your profits can be treated either as capital gains or as business income. This distinction is the single most important factor determining your final tax bill. For most casual investors, only 50% of net capital gains are taxed. For active traders, 100% of profits are taxed as business income at their full marginal rate. Understanding your classification is the first step to mastering your Forex Tax in Canada. This guide, written from over a decade of personal trading experience, will walk you through everything a Canadian trader, whether using an online forex broker or a more traditional platform, needs to know.

Key Takeaways for Canadian Forex Traders

- Taxation is Mandatory: All profits from forex trading in Canada are subject to tax. There are no exceptions for small amounts.

- Two Tax Treatments: The core issue for Forex Tax in Canada is whether your profits are considered capital gains or business income. This classification impacts your tax rate significantly.

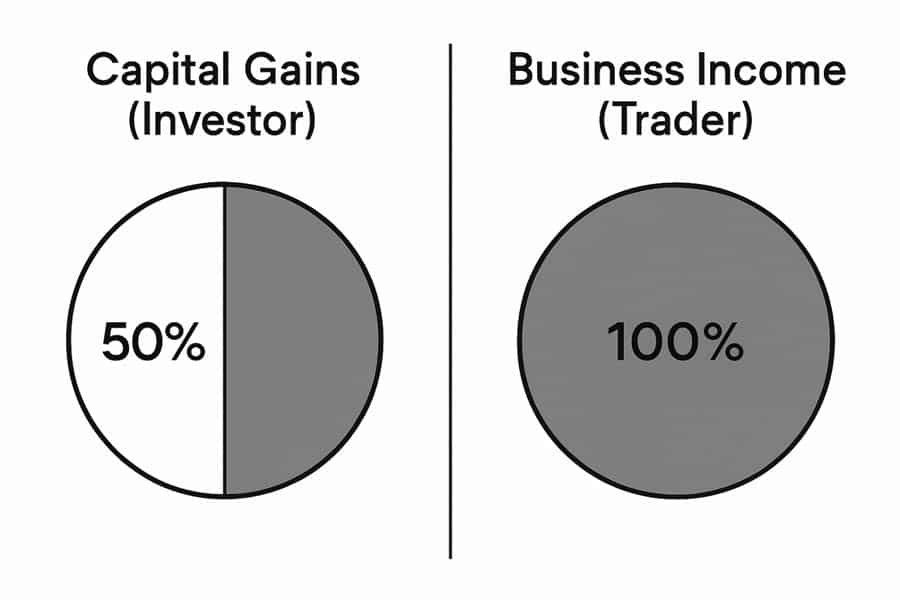

- Capital Gains: If you’re deemed an investor, you pay tax on only 50% of your net capital gains. This is known as the “capital gains inclusion rate.”

- Business Income: If you’re considered a day trader running a business, 100% of your net profit is added to your income and taxed at your marginal rate.

- CRA’s Intent Test: The CRA uses several factors to determine your status, but the primary consideration is your “intention” at the time of the trades. Frequent, short-term trades signal a business-like activity.

- Reporting is Crucial: You must report gains and losses correctly on your tax return—either on Schedule 3 (Capital Gains) or Form T2125 (Business Income). Accurate record-keeping is non-negotiable.

- Losses Have Value: Capital losses can only offset capital gains. Business losses, however, can often be used to offset other sources of income, providing a potential tax shield in unprofitable years.

- Currency Conversion Matters: All transactions must be converted to Canadian dollars (CAD) for reporting purposes. The CRA recommends using the Bank of Canada’s daily exchange rate on the settlement date of each transaction.

Disclaimer: This article provides general information and is not a substitute for professional tax advice. The Canadian tax landscape is complex. Always consult with a qualified accountant or tax lawyer to address your specific financial situation.

Quick-Look Tax Table: Gains vs. Business Income

To immediately clarify the financial impact of your classification, here is a simple comparison. This is the cornerstone of understanding Forex Tax in Canada and planning your trading strategy accordingly. Many new traders overlook this, but as someone who has navigated this for years, I can tell you this table represents the most critical financial fork in the road you’ll face.

| Feature | Forex as Capital Gains (Investor) | Forex as Business Income (Trader) |

| Taxable Portion of Profit | 50% of net gains | 100% of net profit |

| Tax Form for Reporting | Schedule 3 (Capital Gains and Losses) | Form T2125 (Statement of Business or Professional Activities) |

| How Losses Are Treated | Capital losses can only offset capital gains. They can be carried back 3 years or forward indefinitely. | Business losses can offset other income sources (e.g., employment income) in the same year. |

| Expense Deductions | Very limited. Only direct costs of disposition (e.g., some transaction fees) can be claimed. | Broad range of reasonable business expenses are deductible (e.g., software, data feeds, home office). |

| Typical Trader Profile | Holds positions for longer periods (weeks, months, or years). Trading is not their primary activity. | High volume of trades (daily or weekly). Short holding periods. Trading is systematic and commercial. |

Are You an Investor or a Trading “Business”?

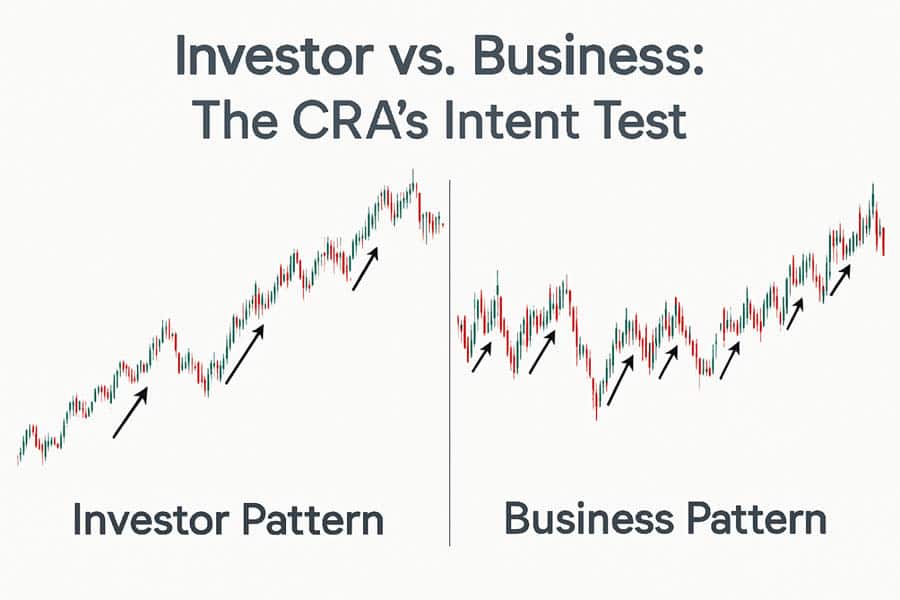

This is the million-dollar question—or at least, the question that determines how many thousands of dollars you’ll owe. The CRA doesn’t have a single, rigid definition, which creates a grey area that many traders find confusing. They look at a collection of factors to determine your intent. In my experience, it’s not about what you call yourself, but what your trading pattern shows. Let’s break down the CRA’s four main tests for capital gains vs business income CRA looks for.

Frequency of Transactions

This is often the most significant factor. Someone making a few forex trades a year is likely to be viewed as an investor. In contrast, a person executing multiple trades every day or week is exhibiting a pattern consistent with a business. If your trading history looks like a busy commercial enterprise, the CRA will likely treat it as one. When I first started, my handful of long-term swing trades clearly fell under capital gains. As I moved to day trading, the sheer volume of my transactions was the clearest indicator that I had crossed into business income territory.

Duration of Ownership

How long do you hold your currency pairs? Investors typically hold assets for longer periods—weeks, months, or even years—hoping for long-term appreciation. A business, on the other hand, aims for quick profits from short-term market fluctuations. If you’re opening and closing positions within the same day (day trading) or within a few days (swing trading), you are behaving like a business, not a passive investor. The rapid turnover of assets is a classic hallmark of commercial activity.

Knowledge and Experience

The CRA considers your level of expertise. Do you have specialized knowledge of the forex markets? Do you use sophisticated charting software and analytical tools? Do you spend a significant amount of time studying market trends? If so, this points toward a business-like approach. A casual investor might buy some USD before a vacation, whereas a dedicated trader subscribes to data feeds, uses a professional-grade forex trading broker, and has a well-defined trading plan. This level of engagement and skill suggests a commercial venture.

Intention to Profit

This test looks at whether your primary intention is to profit from short-term price changes versus long-term investment growth. A business operation is characterized by a systematic and repetitive effort to capture profit from market volatility. If you have a business plan (even an informal one), set daily profit targets, and rely on trading for a portion of your income, the CRA will almost certainly classify your activities as a business. This is a crucial aspect of the forex trading tax in Canada debate.

Read More: Forex Tax in Dubai

Tax Rates 2025: Federal & Provincial Snapshot

Your tax rate depends on your classification (investor vs. business) and your total taxable income for the year. Canada uses a progressive tax system, meaning the more you earn, the higher your tax rate on those additional earnings. Below is a snapshot of the projected 2025 federal tax brackets. Remember to add your provincial tax rate on top of this, as it varies significantly by province.

2025 Federal Income Tax Brackets (Projected)

These rates apply to your total taxable income, which includes either 50% of your net capital gains or 100% of your net business income from forex trading.

| Taxable Income | Federal Tax Rate |

| Up to $55,867 | 15% |

| Over $55,867 up to $111,733 | 20.5% |

| Over $111,733 up to $173,205 | 26% |

| Over $173,205 up to $246,752 | 29% |

| Over $246,752 | 33% |

Example Calculation:

- As an Investor: If you make a $20,000 net profit, it’s treated as a capital gain. Only 50% ($10,000) is taxable. If you’re in the 20.5% federal tax bracket, your federal tax would be $2,050 ($10,000 * 0.205).

- As a Business: If you make a $20,000 net profit, 100% ($20,000) is taxable. In the same 20.5% bracket, your federal tax would be $4,100 ($20,000 * 0.205).

This simple example highlights the massive difference your classification makes. It’s a fundamental concept for anyone dealing with Forex Tax in Canada.

Reporting Forex Gains Step-by-Step

Knowing your tax liability is one thing; correctly reporting it is another. This is where meticulous record-keeping becomes your best friend. From my own early mistakes, I can’t stress this enough: track everything. Here’s a guide on how to report forex income on tax return Canada based on your trader type.

Step 1: Calculate Your Adjusted Cost Base (ACB) and Proceeds

For every single trade, you need to calculate your gain or loss in Canadian dollars (CAD). This is non-negotiable.

- Adjusted Cost Base (ACB): This is the cost of acquiring the currency, including any transaction fees, converted to CAD using the exchange rate on the date of the transaction.

- Proceeds of Disposition: This is the selling price of the currency, converted to CAD using the exchange rate on the date of the settlement.

- Gain or Loss: Proceeds of Disposition – ACB = Your Gain or Loss in CAD.

The CRA states that you should use the exchange rate in effect on the day of the transaction. For consistency, it’s best practice to use the daily average exchange rate provided by the Bank of Canada. Trying to use different conversion methods can be a red flag for auditors.

Step 2: Complete the Correct Tax Form

Your trader classification dictates which form you’ll use.

- Investors (Capital Gains): You will report all your trades on Schedule 3, Capital Gains (or Losses). You list the proceeds, the ACB, and the outlays and expenses to calculate your net capital gain or loss. This net figure is then transferred to line 12700 of your T1 personal income tax return. Remember, only 50% of your net gain is taxable.

- Businesses (Business Income): You must complete Form T2125, Statement of Business or Professional Activities. Here, you report your gross revenue (total proceeds from winning trades) and then deduct your cost of goods sold (total cost of those trades) and all eligible business expenses. The resulting net income (or loss) is then reported on line 13500 (Business income) of your T1 return.

Step 3: Keep Impeccable Records

If you are ever audited, you will need to produce records to support every number on your tax return. Your record-keeping system should be robust. I use a dedicated spreadsheet that tracks:

- Date of trade (opening and closing)

- Currency pair

- Amount bought/sold

- Exchange rate at purchase (CAD)

- Exchange rate at sale (CAD)

- Cost in CAD (ACB)

- Proceeds in CAD

- Net gain/loss in CAD per trade

- Brokerage statements as backup

This level of detail is essential for accurately calculating your Forex Tax in Canada and surviving a potential CRA review.

Legal Ways to Cut Your Forex Tax Bill

Once you understand the rules, you can start to strategize. The goal isn’t tax evasion; it’s tax efficiency. There are several CRA-approved methods to legally minimize your tax burden. Over the years, I’ve used a combination of these to optimize my financial outcomes.

Claimable Expenses for Active Traders

If you qualify for business income treatment, a world of deductions opens up to you. This is one of the biggest advantages of being classified as a business. You can deduct any reasonable expense incurred for the purpose of earning income. Think like a business owner:

- Home Office Expenses: A portion of your rent/mortgage interest, property taxes, utilities, and internet bill, calculated based on the square footage of your dedicated office space.

- Trading Software & Data Fees: Subscriptions to charting platforms (like TradingView or MT4/MT5 add-ons), news feeds, and analytical services.

- Computer & Office Equipment: You can claim capital cost allowance (CCA), which is a depreciation deduction, on computers, monitors, and office furniture.

- Education: Costs for courses, books, or seminars related to improving your trading skills.

- Accounting and Legal Fees: The cost of hiring a professional to help with your taxes or business structure.

These deductions directly reduce your net income, and therefore, your tax bill. This is a key part of managing your Forex Tax in Canada effectively.

Using Corporations & RRSP/TFSA Shields

For highly profitable traders, incorporating can be a powerful tax-deferral strategy. By setting up a Canadian-controlled private corporation (CCPC), you can trade within the corporation. The profits are taxed at the small business tax rate (which is often much lower than personal marginal rates). You then only pay personal income tax when you pay yourself a salary or dividend from the corporation. This allows you to control the timing and amount of your personal income. However, setting up and maintaining a corporation involves costs and administrative complexity, so it’s generally only worthwhile for those with substantial six-figure profits. It’s a significant step in your journey with forex trading tax in Canada.

What about Tax-Free Savings Accounts (TFSAs) and Registered Retirement Savings Plans (RRSPs)? The CRA has a clear stance: if you are frequently trading forex within a TFSA or RRSP, they can deem this to be “carrying on a business.” If this happens, the tax-sheltered status is revoked for those activities, and the profits become fully taxable. For this reason, these registered accounts are generally not suitable for active forex day trading.

Foreign Tax Credit & Record-Keeping Hacks

If your online forex broker is located outside Canada and withholds any tax on your profits (which is rare for forex but possible with other investments), you may be able to claim a foreign tax credit to avoid double taxation. This prevents you from paying tax on the same income to both a foreign government and the CRA.

My biggest “hack” for record-keeping is automation. Don’t wait until tax season. Use software or a detailed, formula-driven spreadsheet to update your trades weekly. Download your broker statements monthly and reconcile them. By the time April comes around, your work is 90% done. This discipline turns a monumental task into a manageable habit and is the best defense against a CRA audit.

Read More: Tax Implications of Forex Trading

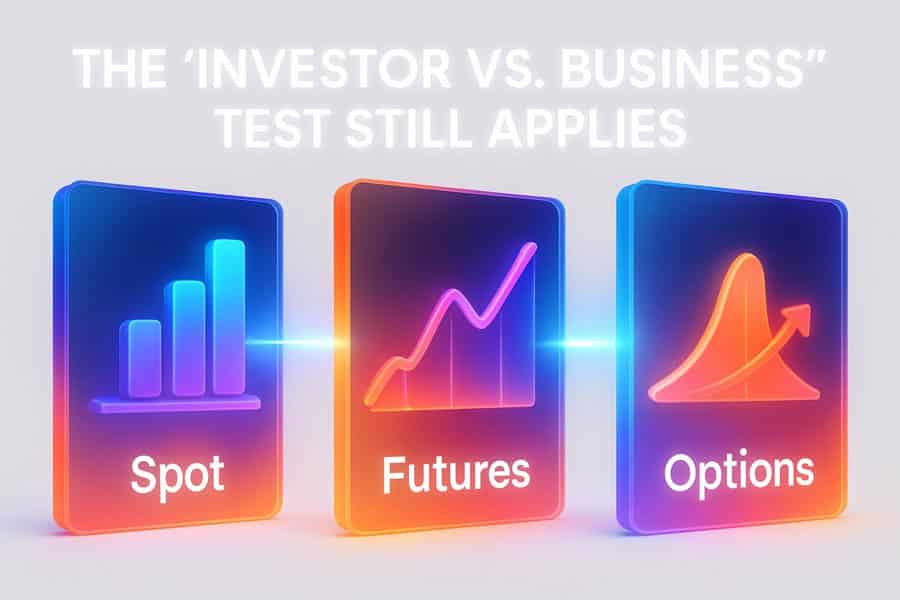

Spot, Futures, Options: Different CRA Treatment?

While the vast majority of retail forex trading in Canada is done in the spot market, some traders use derivatives like futures and options. Does the CRA treat them differently? Generally, the core principles of “investor vs. business” still apply. However, there can be nuances.

- Spot Forex: This is the direct buying and selling of currencies. The tax treatment hinges entirely on the capital gains vs. business income factors we’ve discussed.

- Forex Futures: These are contracts to buy or sell a currency at a predetermined price on a future date. They are typically traded on regulated exchanges. The CRA’s guidance on futures often leans toward business income due to the inherent leverage and speculative nature, but capital gains treatment is still possible if the trading pattern supports it.

- Forex Options: An option gives the right, but not the obligation, to buy or sell a currency. The tax treatment can be complex. The premium paid for an option is a capital outlay. If the option expires worthless, it’s a capital loss. If exercised, the premium is factored into the cost base of the acquired currency. Again, high-frequency options trading will be viewed as a business.

For most traders, regardless of the instrument, the answer to the Forex Tax in Canada question comes back to the same set of facts: your frequency, holding period, and intent.

Common Mistakes That Trigger CRA Audits

Having been in the trading community for years, I’ve seen fellow traders make costly mistakes. An audit is stressful, time-consuming, and can be expensive. Here are the most common red flags to avoid:

- Not Reporting at All: This is the biggest mistake. The CRA receives information from financial institutions, including many international brokers, through information-sharing agreements. They will eventually find out. Failing to report can lead to severe penalties and interest charges.

- Misclassifying Income: Deliberately reporting obvious business income as capital gains to take advantage of the 50% inclusion rate is a major trigger for audits. Be honest and consistent in your classification.

- Sloppy Record-Keeping: If you claim business income but have no organized records or receipts for your expenses, the CRA will likely disallow them. Your bank statements are not enough; you need detailed logs.

- Inconsistent Currency Conversion: Using different FX conversion methods from one year to the next or even within the same year can signal an attempt to manipulate gains or losses. Stick to one method, preferably the Bank of Canada daily rate.

- Claiming a TFSA for Day Trading: As mentioned, using a TFSA for high-frequency forex trading is a known red flag for the CRA and can lead to a reassessment where all gains are taxed as business income.

Avoiding these pitfalls is critical for anyone serious about managing their Forex Tax in Canada and maintaining a clean record with the revenue agency.

Read More: Forex Tax in India

Unlock Your Trading Potential with a Trusted Broker

Choosing the right regulated forex broker is as crucial as your tax strategy. Opofinance, regulated by ASIC, offers a robust environment for Canadian traders looking to elevate their game.

- Advanced Trading Platforms: Access popular platforms like MT4, MT5, cTrader, and the proprietary OpoTrade app to suit your trading style.

- Innovative AI Tools: Leverage cutting-edge technology with an AI Market Analyzer, AI Coach, and 24/7 AI Support to make more informed decisions.

- Diverse Trading Options: Explore Social Trading to follow experts or take on Prop Trading challenges to trade with firm capital.

- Secure & Flexible Transactions: Enjoy peace of mind with safe and convenient deposits and withdrawals, including crypto payments with zero transaction fees.

Ready to trade with a broker that provides the tools and security you need? Explore Opofinance today!

Conclusion

Navigating Forex Tax in Canada doesn’t have to be intimidating. It boils down to one key decision: are your activities considered investing (capital gains) or a business? Once you determine this based on your trading patterns, the path becomes clearer. Always maintain meticulous records, convert every transaction to CAD, and report your income using the correct forms. By treating your trading with professionalism, you can stay compliant with the CRA, minimize your tax burden legally, and focus on what you do best: trading.

Can I claim forex losses against my employment income in Canada?

Only if your trading is classified as a business. Business losses can be used to offset other sources of income. If your trading is classified as generating capital gains, your capital losses can only be used to offset capital gains.

Do I need a GST/HST number for forex trading in Canada?

No. Financial services, including spot forex trading, are generally exempt from GST/HST. You do not need to register for or collect these taxes on your trading profits.

What happens if I forget to report forex income from a previous year?

You should amend your previous tax return as soon as possible through the CRA’s Voluntary Disclosures Program (VDP). This program allows you to correct inaccurate or incomplete information, potentially avoiding penalties or prosecution if you come forward before the CRA contacts you.

Is there a minimum profit amount before I have to pay tax?

No, there is no minimum. You are required to report all income, no matter how small. However, your total income for the year must exceed the basic personal amount (a tax-free threshold) before you actually owe any federal tax.

How does the CRA know about my offshore forex broker account?

The CRA uses the Common Reporting Standard (CRS), an international agreement for the automatic exchange of financial account information between tax authorities. Over 100 countries participate, meaning your offshore broker is likely required to report your account details to the CRA.