Navigating the world of foreign exchange is complex enough without the added headache of taxes. The critical question for any UK-based trader, from novice to seasoned professional, is how your profits are treated by His Majesty’s Revenue and Customs (HMRC). Answering the question of forex tax in UK is central to your trading strategy and profitability. Whether you’re speculating with a regulated forex broker or managing a diverse portfolio, understanding your tax obligations is non-negotiable. This guide breaks down everything you need to know, from whether forex is tax-free to calculating your liabilities and planning for the 2025/26 tax year.

Key Takeaways

- Not Always Tax-Free: While spread betting on forex is typically free from Capital Gains Tax (CGT) and stamp duty, HMRC can reclassify it as trading income if it’s your primary source of income. Trading forex CFDs is almost always liable for CGT.

- Three Classifications: HMRC categorises forex activities into three main types: speculative (like spread betting, usually tax-free), private investor (subject to CGT at 10%/20%), or self-employed trader (subject to Income Tax at 20%-45%).

- Shrinking Allowances: The Capital Gains Tax Annual Exempt Amount (AEA) for the 2024/25 tax year is just £3,000. It’s a significant drop from previous years, making more profits taxable.

- Losses Are Valuable: You can offset allowable capital losses against your capital gains to reduce your overall tax bill. Meticulous record-keeping is essential to prove these losses.

- Major Non-Dom Changes: The new Foreign Income and Gains (FIG) regime starting April 2025 will significantly alter how non-domiciled individuals are taxed on their forex profits.

- Record-Keeping is Crucial: Regardless of your classification, maintaining detailed records of every trade, including size, currency pair, entry/exit prices, and P&L, is vital for compliance with forex tax in UK regulations.

Disclaimer: The information provided in this article is for informational purposes only and does not constitute personal financial or tax advice. Tax laws are complex and subject to change. You should consult with a qualified, independent tax adviser or contact HMRC directly to understand how the rules apply to your specific circumstances.

Is Forex Trading Tax-Free or Taxable in the UK?

This is the most common question I hear, and the answer is not a simple yes or no. The idea that all forex trading is tax-free in the UK is a dangerous myth. The tax treatment of your profits depends entirely on two factors: the financial instrument you use (e.g., spread bets vs. CFDs) and how HMRC classifies your trading activity. For most retail traders, the profits are taxable. The key phrase is “it depends.” While a specific type of forex derivative—spread betting—is often tax-free, this isn’t a blanket exemption for all forex activities. Answering “is forex trading tax-free in UK?” requires a look at your personal trading patterns and the products you trade.

Quick-Glance Tax Matrix (Spread Betting vs CFDs vs Pro)

To simplify the initial confusion, here is a quick reference table. This matrix provides a clear overview of the default tax treatment for the most common ways people trade forex in the UK. However, remember the nuance: HMRC can reclassify your activities based on their “badges of trade” test, which we’ll cover next.

| Activity Type | Default Tax Treatment | Key Considerations |

| Financial Spread Betting | Tax-Free (treated as betting) | No Capital Gains Tax (CGT) No Stamp Duty Losses cannot be offset against other gains Can be reclassified as income if it’s your sole, structured source of funds |

| CFD/Spot Forex Trading (as an Investor) | Capital Gains Tax (CGT) | Taxable at 10% (basic rate) or 20% (higher rate) Annual Exempt Amount of £3,000 (2024/25) applies Allowable losses can be offset against other capital gains This is the most common classification for retail traders |

| Self-Employed / Professional Trading | Income Tax & National Insurance | Taxable at income tax bands (20%, 40%, 45%) Class 2 and Class 4 National Insurance Contributions (NICs) apply Allowable business expenses can be deducted Triggered by the “badges of trade” test |

HMRC’s decision to re-classify you from a private investor to a self-employed trader isn’t arbitrary. It’s based on a holistic view of your activities. If you trade with a high frequency, in a systematic and organised manner, with the clear intention of making a living from it, you risk being seen as a professional trader for tax purposes. This is a crucial distinction in the world of forex tax in UK.

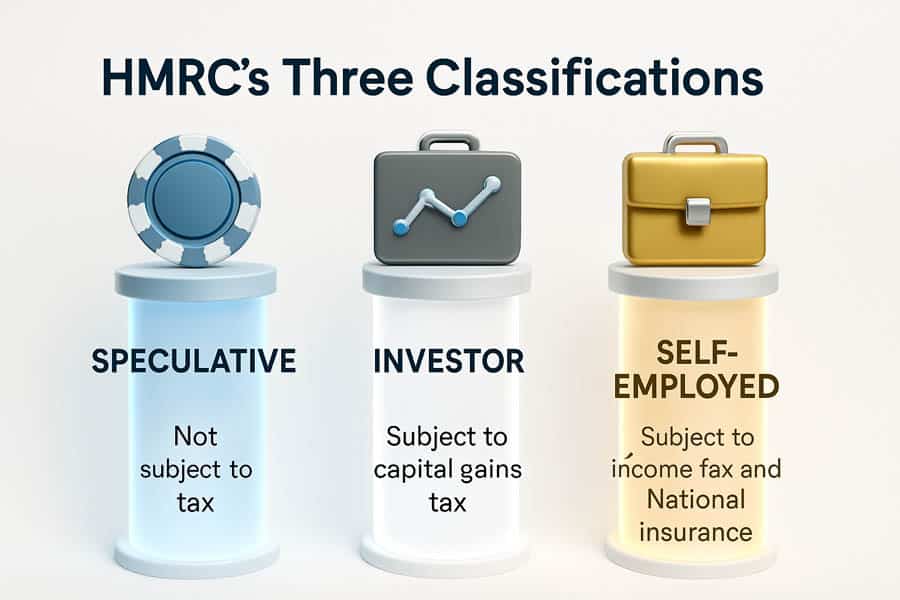

HMRC’s Three Classifications & Your Bill

Understanding which category you fall into is the first step to mastering your forex tax in UK. HMRC doesn’t have a single, rigid definition for a “forex trader.” Instead, it looks at your behaviour and intentions to place you into one of three buckets. Each has vastly different tax implications.

Speculative (Gambling)

This is the default classification for financial spread betting. Because it’s legally defined as wagering, any profits you make are considered winnings and are therefore tax-free. This is the primary appeal of spread betting for many UK traders. However, there’s a significant catch: if your spread bets result in a loss, you cannot offset those losses against any other taxable gains. The taxman gives with one hand and takes with the other. It’s a high-stakes game where the tax-free status comes at the cost of any relief for your losses.

Investor (Capital Gains)

This is the most common category for individuals trading Contracts for Difference (CFDs) or spot forex through a broker. HMRC views you as a private investor managing your own portfolio. As such, your net profits are subject to Capital Gains Tax (CGT). For the 2024/25 tax year, the CGT rates on forex profits are 10% if you are a basic-rate income taxpayer and 20% if you are a higher or additional-rate taxpayer. You can also utilise the Annual Exempt Amount (AEA), which is £3,000 for 2024/25. Any net gains below this threshold are tax-free. This is the core of the capital gains tax on forex profits UK system.

Self-Employed Trader

If your trading becomes more than just a side activity, you might be classified as self-employed. This typically happens when your trading is frequent, systematic, and your primary source of income. HMRC uses the “badges of trade” test to determine this (more on that below). If you are deemed to be trading as a business, your profits are no longer treated as capital gains. Instead, they are subject to Income Tax at your marginal rate (20%, 40%, or 45%) and you’ll also have to pay Class 2 and Class 4 National Insurance Contributions (NICs). While this sounds punitive, it does mean you can deduct a wider range of expenses, similar to any other small business.

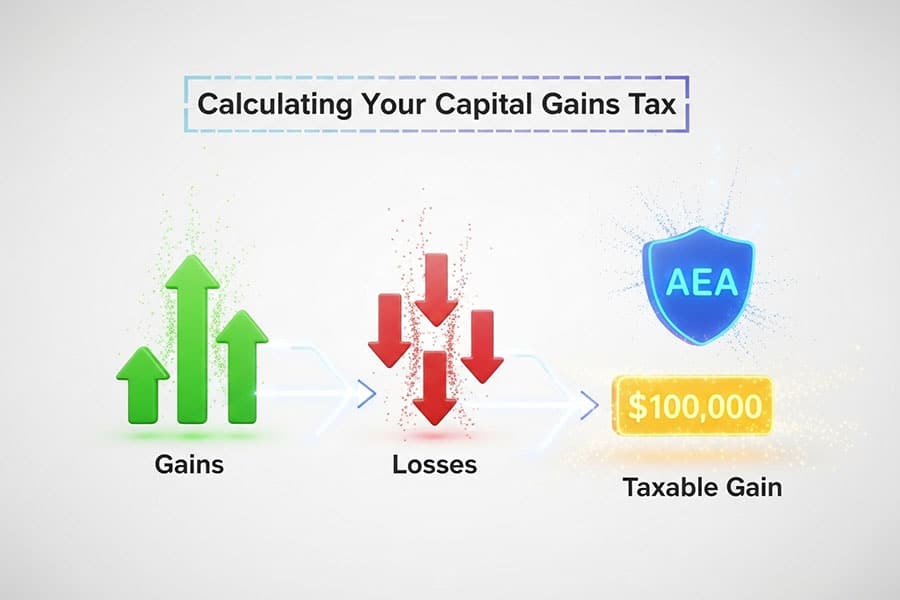

Step-by-Step: Calculating CGT on Forex Profits

For most retail forex traders using CFDs, calculating your Capital Gains Tax liability is a key annual task. It can seem daunting, but it’s a logical process. I learned early on that breaking it down into simple steps removes the fear. Thinking about capital gains tax on forex profits UK is much easier when you have a clear framework.

- Sum All Your Gains and Losses: Go through your trading account statement for the tax year (6th April to 5th April). Add up the profit from every single winning trade and, separately, add up the loss from every losing trade. This includes overnight financing fees (swaps), which are an allowable cost.

- Calculate Your Net Position: Subtract your total allowable losses from your total gains. If you have more gains than losses, you have a net capital gain. If you have more losses than gains, you have a net capital loss, which you can carry forward to offset against future gains.

- Deduct the Annual Exempt Amount (AEA): Subtract the AEA from your net capital gain. For the 2024/25 tax year, this is £3,000. If your net gain is less than £3,000, you have no CGT to pay.

- Apply the Correct Tax Rate: The remaining amount is your taxable gain. If your total taxable income (including these gains) falls within the basic-rate income tax band, you pay CGT at 10%. If it pushes you into the higher-rate band, you pay CGT at 20% on the portion of the gain that falls into that band.

A Real-World Calculation Example

Let’s make this tangible. Imagine a trader, Sarah, who is a higher-rate taxpayer. In the 2024/25 tax year:

- Total profits from winning CFD trades: £15,000

- Total losses from losing CFD trades: £6,000

- Total swap fees paid: £500

Step 1 & 2: Calculate Net Gain

Her total allowable losses are £6,000 + £500 = £6,500.

Her net capital gain is £15,000 (gains) – £6,500 (losses) = £8,500.

Step 3: Deduct the AEA

Her taxable gain is £8,500 (net gain) – £3,000 (AEA) = £5,500.

Step 4: Apply Tax Rate

As a higher-rate taxpayer, Sarah pays CGT at 20%.

Her CGT liability is £5,500 20% = £1,100.

This simple calculation demonstrates the direct impact of understanding the forex tax in UK. Without tracking her swap fees, Sarah would have paid tax on an extra £500 of gains.

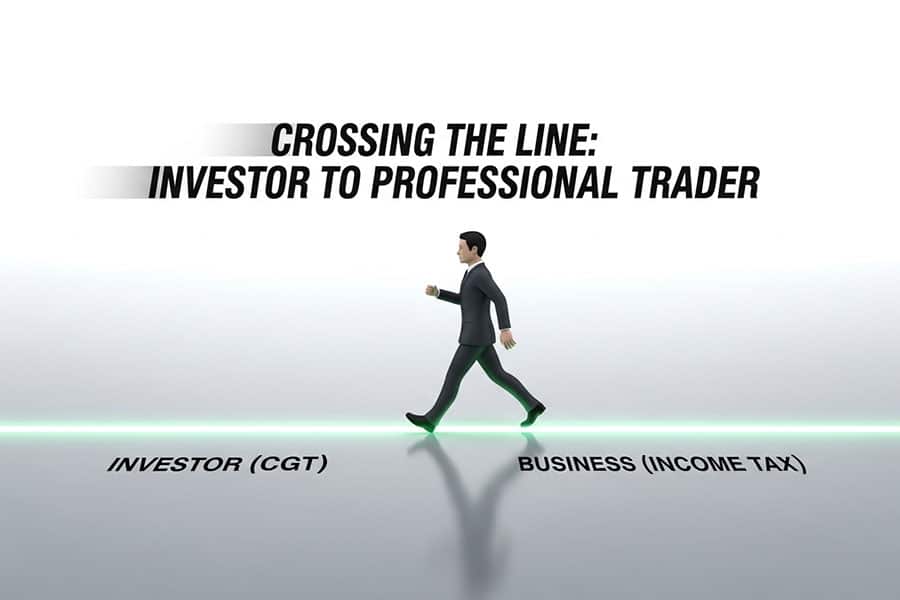

Full-Time Trading? When Income Tax & NICs Kick In

The dream for many is to trade forex full-time. However, this transition carries significant tax implications. Once trading becomes your main business, you cross the line from being an ‘investor’ to a ‘self-employed trader’ in HMRC’s eyes. This shift is determined by the “badges of trade,” a set of criteria HMRC uses to assess whether an activity constitutes a business.

The ‘Badges of Trade’ Test

There is no single factor that makes you a professional trader; it’s about the overall picture. Here are the key “badges” HMRC looks for:

- Profit-Seeking Motive: Is your primary goal to make a profit? For almost all traders, the answer is yes.

- Number of Transactions: Are you making a high volume of trades? A few trades a year is an investment; hundreds or thousands suggest a business.

- Nature of the Asset: Forex pairs are not typically held for pride of ownership or personal enjoyment. They are speculative assets, which points towards trading.

- Connection to Existing Trade: Is the trading related to your existing profession? (Less relevant for most retail forex traders).

- Financing: Are you using short-term financing or leverage to fund your trades? This is a strong indicator of trading.

- Length of Ownership: Are you holding positions for minutes, hours, or days, rather than months or years? Short holding periods are a classic sign of trading, not investing.

- Organisation: Do you have a business plan, dedicated office space, and sophisticated software? This level of organisation points towards a business.

If you tick several of these boxes, you will likely need to register as self-employed and handle your forex tax in United Kingdom through Self Assessment as trading income.

Record-Keeping Checklist for Full-Time Traders

From my own experience, meticulous record-keeping is non-negotiable once you go professional. It’s the only way to accurately calculate your profits and justify your expenses to HMRC. Here’s a checklist:

- Trade Log: A detailed spreadsheet or software export showing date, time, currency pair, position size, entry price, exit price, and gross P&L for every trade.

- Broker Statements: Download and archive all monthly and annual statements from your broker.

- Expense Receipts: Keep digital or physical copies of every single business-related expense.

- Bank Statements: It’s wise to have a separate bank account for your trading business to easily track cash flow.

“HMRC’s default position is to tax, so the onus is always on the taxpayer to prove otherwise with clear, contemporaneous records. Never underestimate the power of a well-maintained spreadsheet.” – John Davies, Chartered Tax Adviser

Allowable Expenses Most Traders Miss

One of the upsides of being taxed as a business is the ability to deduct allowable expenses. Many new full-time traders underclaim. Here are some commonly missed deductions:

- Data Feeds & Software: Subscriptions to platforms like TradingView, news squawks, or specialist charting software.

- Home Office Costs: A proportion of your household bills (rent/mortgage interest, council tax, utilities, broadband) based on the space you use for trading.

- Computer Equipment: The cost of laptops, monitors, and other hardware used for trading.

- Education: Fees for trading courses, books, and seminars that improve your existing skills.

- Bank Charges: Fees associated with your trading bank account.

Spread Betting: The Tax-Free Lure & Hidden Catch

Financial spread betting is hugely popular in the UK, primarily because the profits are generally free from Capital Gains Tax and stamp duty. For many, it’s the simplest way to speculate on forex movements without worrying about a complex tax return. However, it’s crucial to understand why it’s tax-free and what the limits are.

The “tax-free” status comes from its legal classification as betting. You are not buying or selling an underlying asset; you are wagering on the direction of its price movement. This distinction is vital. But here lies the hidden catch: HMRC reserves the right to challenge this classification if your activities mirror those of a professional trader. If you rely on spread betting for your regular income, have no other job, and trade in a highly systematic way, HMRC could argue you are, in fact, running a trading business. In such a rare case, your profits could be reclassified as taxable income. This is a grey area, but one to be aware of if you plan to make spread betting your sole endeavour. The limitation on loss relief also remains a significant drawback.

Limited Company Route: Corporation Tax & Planning

For highly profitable and established traders, operating through a limited company can be an effective tax planning strategy. Instead of paying Income Tax on all profits as a sole trader, your business pays Corporation Tax on its profits. You then have flexibility in how you extract money from the company.

The main Corporation Tax rate is 25%, but a small profits rate of 19% applies to companies with profits of £50,000 or less. You can then pay yourself a combination of a small, tax-efficient salary and dividends. Dividends have their own tax-free allowance (£500 for 2024/25) and are taxed at lower rates than income tax (8.75%, 33.75%, 39.35%). This allows for sophisticated planning to minimise your personal tax bill. However, running a company comes with increased administrative burdens, costs, and director’s responsibilities. It is essential to weigh these against the potential tax savings. Also, be aware of the Making Tax Digital for Income Tax Self Assessment (MTD ITSA) rules coming into effect from 2026, which will require digital records and quarterly updates for sole traders and landlords, reinforcing the need for robust digital bookkeeping for all serious traders.

New 2025 FIG Regime for Non-Doms: What to Know

The UK’s tax landscape for non-domiciled individuals is undergoing a seismic shift from 6th April 2025. The old “remittance basis” of taxation is being abolished and replaced with a new four-year Foreign Income and Gains (FIG) regime. This has major implications for non-doms trading forex.

Under the new system, qualifying individuals who become UK residents will not pay UK tax on their foreign income and gains for the first four years of residency. This means a non-dom forex trader could potentially trade with an offshore broker on non-UK currency pairs and pay no UK tax on the profits for that initial four-year period, regardless of whether the money is brought into the UK. After the four years, they will be taxed on their worldwide income and gains in the same way as other UK residents. There are transitional provisions, including a 12% Temporary Repatriation Facility (TRF) for remitting old foreign income and gains, and potential rebasing of assets for CGT purposes. Understanding this new regime is critical for any non-dom involved in the forex tax in UK ecosystem.

Reporting Deadlines, Forms & Digital Tools

Staying compliant means knowing how, what, and when to report to HMRC. Missing deadlines can result in penalties and interest, so organisation is key.

- Self Assessment: If you have CGT to pay or are classified as a self-employed trader, you must register for Self Assessment. The main form is the SA100, and you’ll need to complete supplementary pages, typically the SA108 for capital gains and the SA103 for self-employment.

- Key Deadlines: The deadline to register for Self Assessment is 5th October after the end of the tax year in which you had the liability. The deadline for online tax returns and paying the tax you owe is midnight on 31st January the following year.

- Digital Tools: HMRC offers an online Capital Gains Tax service. While it’s primarily designed for reporting gains on UK residential property within 60 days, it’s an example of their move towards digital. For most forex traders, the annual Self Assessment return remains the primary reporting method.

- Platform Exports: A lesson I learned the hard way is that relying solely on your broker’s platform export is not enough. While essential, you need to consolidate data if you use multiple brokers and ensure it’s in a format HMRC would understand. I reconcile my platform exports with my own trade log and bank statements to create a single, definitive source of truth for my tax return. This diligence is crucial for anyone serious about managing their forex tax in UK.

Seven Proven Ways to Legally Reduce Your Forex Tax Bill

Effective tax planning is just as important as a good trading strategy. Here are seven legitimate ways to potentially lower your forex tax liability in the UK.

- Offset Capital Losses: This is the most fundamental tax-saving tool. Don’t just report your gains. Meticulously track every loss, including commissions and swap fees. You can offset current year losses against current year gains. Any excess loss can be carried forward indefinitely to offset against future gains.

- Use Your Spouse’s Allowances: If your spouse or civil partner is in a lower tax band or hasn’t used their Annual Exempt Amount, you could transfer assets to them before a sale to crystallise a gain in their name. This must be a genuine, outright gift.

- Strategic Use of Spread Betting: While not a long-term solution for a career, using spread betting for short-term speculative trades or hedges can be a tax-efficient strategy, as profits are typically tax-free.

- Pension Contributions: Making personal contributions to a registered pension scheme extends your basic-rate tax band. This can mean that a portion of your capital gain that would have been taxed at 20% is instead taxed at 10%.

- ISA-Wrapped FX ETFs: For longer-term currency views, consider holding a currency-focused Exchange Traded Fund (ETF) within a Stocks and Shares ISA. Any gains or income generated within an ISA are completely tax-free. You cannot hold CFDs or spread bets in an ISA.

- Limited Company Profit Deferral: If you operate through a limited company, you can choose when to extract profits. In a highly profitable year, you can leave funds in the company (paying Corporation Tax) and draw them down as dividends in a future, less profitable year to manage your personal tax liability.

- Trade in USD (Non-Doms under FIG): A pro-tip for non-doms under the new FIG regime: if your capital is already in USD and you trade with an offshore broker, keeping your P&L in USD can simplify things. It avoids creating a separate taxable event on the currency conversion back to sterling, keeping the gain clearly defined as a “foreign gain” during your initial four-year window.

Experience Advanced Trading with Opofinance

Ready to elevate your trading journey? As an ASIC-regulated broker, Opofinance offers a secure and innovative environment tailored for traders who demand more. Gain your edge with our advanced tools and platforms.

- Advanced Trading Platforms: Choose from MT4, MT5, cTrader, and the intuitive OpoTrade platform.

- Innovative AI Tools: Leverage our AI Market Analyzer, AI Coach, and 24/7 AI Support to inform your strategy.

- Social & Prop Trading: Join a community of traders and explore funded trading opportunities.

- Secure & Flexible Transactions: Enjoy safe and convenient deposits and withdrawals, including crypto payments with zero fees.

Discover a smarter way to trade. Open your account with Opofinance today.

Conclusion: Key Takeaways & Action Checklist

Effectively managing your forex tax in UK is a fundamental part of being a successful trader. Ignoring it is not an option. The core message is that while profits from spread betting are often tax-free, gains from CFD and spot forex trading are taxable under the Capital Gains Tax regime for most individuals. For dedicated, full-time traders, these profits can be treated as income. With allowances shrinking, meticulous record-keeping and proactive tax planning are more critical than ever.

- Disclaimer: This article is for informational purposes only. Tax laws are subject to change and individual circumstances vary. Always seek advice from a qualified tax professional or consult HMRC guidance to ensure you are compliant.

Action Checklist Before 5 April

- Collate all trading statements for the tax year.

- Calculate your total gains and total allowable losses (including fees).

- Determine your net capital gain or loss.

- Check if you have any losses from previous years to carry forward.

- Register for Self Assessment by 5th October if you have a tax liability.

- Plan to file and pay your tax bill by 31st January.

Do I pay tax on forex profits under £1,000?

If your total net capital gains from all assets (including forex) in a tax year are under the £3,000 Annual Exempt Amount (for 2024/25), you won’t have any Capital Gains Tax to pay. The £1,000 allowance is the Trading Allowance, which applies if you are taxed as a self-employed trader.

How does HMRC know about my forex gains?

HMRC has wide-reaching information-gathering powers. Under agreements like the Common Reporting Standard (CRS), financial institutions and brokers around the world are required to share information about UK residents’ accounts with HMRC. It is a mistake to assume they will not find out.

What happens if I trade with an offshore broker?

Your UK tax liability is based on your residency status, not your broker’s location. If you are a UK resident, you are legally required to declare your worldwide income and gains, including profits from an offshore broker, on your UK tax return.

Can I claim losses from spread betting?

No. Because spread betting profits are tax-free, the flip side is that you cannot claim any relief for your losses. They cannot be used to offset any other capital gains or income.

Is forex trading income or a capital gain?

For most retail traders, it’s a capital gain. However, if you trade with high frequency and it’s your main source of income, HMRC can classify it as income from self-employment based on the “badges of trade” test. This is a crucial distinction for your forex tax in UK liability.