Wondering about your forex tax in Nigeria? Yes, profits from currency trading are taxable. You must declare your net gains as Capital Gains and pay a 10% tax to the Federal Inland Revenue Service (FIRS). Navigating this requires proper record-keeping and understanding the filing process, especially with potential 2025 rule changes on the horizon. Finding a reliable, regulated forex broker is your first step. This guide covers everything from calculating your tax liability to FIRS compliance and smart strategies for traders.

Key Takeaways

- Core Obligation: Forex profits are subject to a 10% Capital Gains Tax (CGT) in Nigeria.

- Who Pays: Any individual resident in Nigeria making a profit from forex trading is liable.

- Filing Body: All tax filings and payments are made to the Federal Inland Revenue Service (FIRS).

- Key Formula: Tax = (Total Profits – Total Losses – Allowable Expenses) x 10%.

- Crucial Practice: Meticulous record-keeping of all trades (deposits, withdrawals, P&L statements) is non-negotiable for accurate reporting and audit defense.

- 2025 Outlook: Stay informed about the Finance (Amendment) Bill 2024, as evolving regulations on foreign exchange gains could impact future compliance.

- Filing Deadline: Annual tax returns are typically due by June 30th of the following year.

Disclaimer: This article provides general information and is not a substitute for professional legal or tax advice. Tax laws are complex and subject to change. Please consult with a qualified tax advisor or legal professional in Nigeria to address your specific financial situation.

Forex tax in Nigeria Explained

For years, I’ve seen a cloud of confusion hang over the topic of forex tax in Nigeria. Many traders, both new and experienced, operate in a grey area, unsure of their obligations. Let’s clear the air. The Nigerian government, through the FIRS, unequivocally views profits from forex trading not as regular income, but as capital gains. This is a critical distinction that shapes your entire approach to tax compliance.

This guide is built from years of personal trading experience and countless hours spent deciphering tax codes and consulting with financial experts. My goal is to give you a practical, step-by-step framework to manage your forex tax obligations confidently and efficiently, ensuring you stay on the right side of the law.

How to Pay Forex Tax in 5 Steps

- Consolidate Your Records: Gather all trading statements from your broker(s) for the financial year (Jan 1st – Dec 31st). This must include every single trade, deposit, and withdrawal.

- Calculate Your Net Capital Gain: Sum up all your winning trades to get your total profit. Then, sum up all your losing trades. Subtract the total losses from the total profits. Also, deduct any allowable expenses. The result is your net capital gain.

- Determine Your Tax Liability: Calculate 10% of your net capital gain. This is the amount of Capital Gains Tax (CGT) you owe to the FIRS.

- File Your Tax Return: Use the FIRS TaxPro-MAX platform to file your annual personal income tax return. You will declare your forex earnings under the Capital Gains section.

- Make Payment: Pay the calculated tax amount through one of the FIRS-approved channels, such as Remita, and obtain a receipt for your records.

Do Forex Traders Pay Tax?

This is the most common question I get, and the answer is a straightforward yes. If you are a resident in Nigeria and you are making a profit from trading forex, you are legally required to pay tax on those earnings. The idea that forex trading exists in a lawless digital space is a costly myth. The FIRS has become increasingly sophisticated in its ability to track financial flows, and non-compliance can lead to severe consequences.

The specific tax applicable is the Capital Gains Tax (CGT), levied at a rate of 10% on your net profits. It’s not on your total revenue or your account balance; it’s on the actual profit you realize after closing your positions and accounting for losses. This is a crucial point many traders miss. You aren’t taxed on unrealized “paper” profits. You are taxed on the real money you’ve made. Understanding the answer to “do forex traders pay tax in Nigeria” is the first step toward responsible and sustainable trading.

The 10% Capital Gains Rule

The governing law here is the Capital Gains Tax Act. It stipulates that a 10% tax is charged on gains accruing from the disposal of chargeable assets. While traditionally applied to assets like real estate or stocks, the FIRS’s interpretation extends this to financial instruments, including foreign currencies traded for profit. Your profit from closing a currency pair trade is considered a ‘disposal’ of that asset, triggering the CGT. Therefore, every successful trader must factor this 10% into their financial planning.

2025 Rule Changes to Know

The financial landscape in Nigeria is dynamic, and staying ahead of regulatory shifts is key to long-term success. While the core forex tax in Nigeria remains a 10% CGT for individuals, recent legislative discussions in 2024 and 2025 signal a much stronger focus from the government on foreign exchange transactions. As a trader, you need to pay close attention to these developments.

I’ve learned that what happens at the corporate level often trickles down to individuals. The headlines about a “windfall levy” on banks’ forex gains and the ongoing debates surrounding the Finance (Amendment) Bill 2024 are clear indicators. They show the government is actively seeking to shore up revenue from forex markets. While these specific bills primarily target banks, they create a precedent and sharpen the FIRS’s focus on all forex-related income, making Nigeria tax compliance for individual traders more critical than ever.

The Finance Amendment Bill

The proposed Finance (Amendment) Bill contains numerous adjustments to Nigeria’s tax laws. For forex traders, the most significant aspect is the overall theme of closing tax loopholes and enhancing scrutiny on foreign currency dealings. It reinforces the need to declare forex income transparently. The bill underscores the government’s intent to formalize tax collection from every possible stream, and the multi-trillion naira forex market is squarely in its sights. It’s a clear signal to get your house in order.

What the Windfall Tax Means

The proposed windfall tax on banks’ FX revaluation gains is a separate issue but reflects the same regulatory mood. It shows that the government is willing to introduce new, targeted taxes to capture what it deems to be excessive profits from currency fluctuations. While this doesn’t directly apply to your retail trading profits today, it sets a tone. It means FIRS forex trading guidelines could become more stringent and audits more common in the coming years.

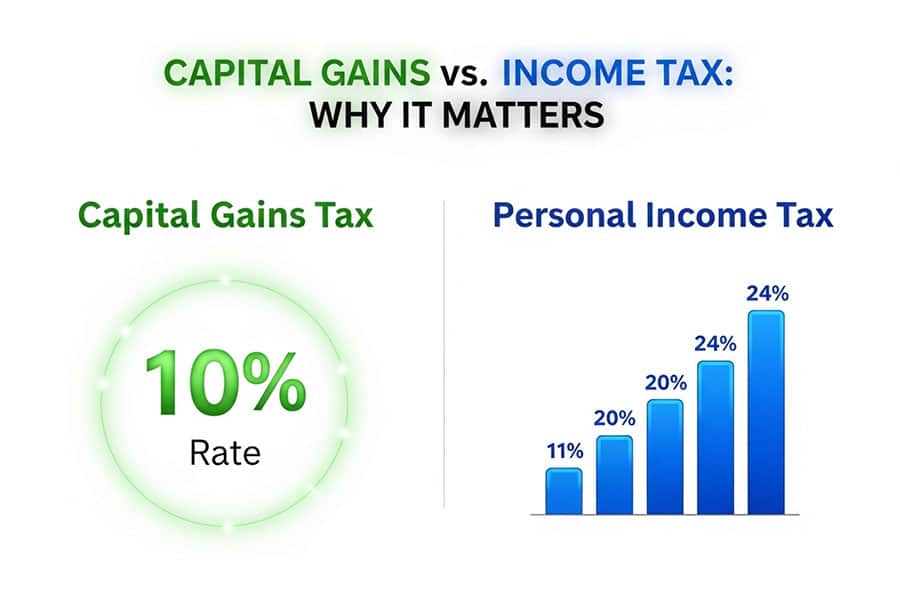

Capital Gains vs. Income Tax

A frequent point of confusion is whether forex profits should be filed under Personal Income Tax (PIT) or Capital Gains Tax (CGT). This is arguably the most important technical detail to get right. I’ve seen traders mistakenly lump their forex earnings with their salary, which is incorrect and can lead to paying a much higher tax rate.

Personal Income Tax in Nigeria is progressive, with rates going up to 24%. In contrast, Capital Gains Tax is a flat 10%. By correctly classifying your trading profits as capital gains, you ensure you are paying the legally correct (and lower) rate. The FIRS considers your trading activity as the buying and selling of an asset (currency), not as a service or employment. This asset disposal framework is what squarely places it under the capital gains tax on forex profits.

Why the Distinction Matters

Getting this wrong can be a costly mistake. Imagine you make a ₦2,000,000 profit. If you incorrectly file it as additional income, you could be taxed at a much higher marginal rate. If filed correctly as a capital gain, you pay a flat ₦200,000 (10%). This distinction is fundamental to proper forex tax in Nigeria management. It ensures you are compliant without overpaying.

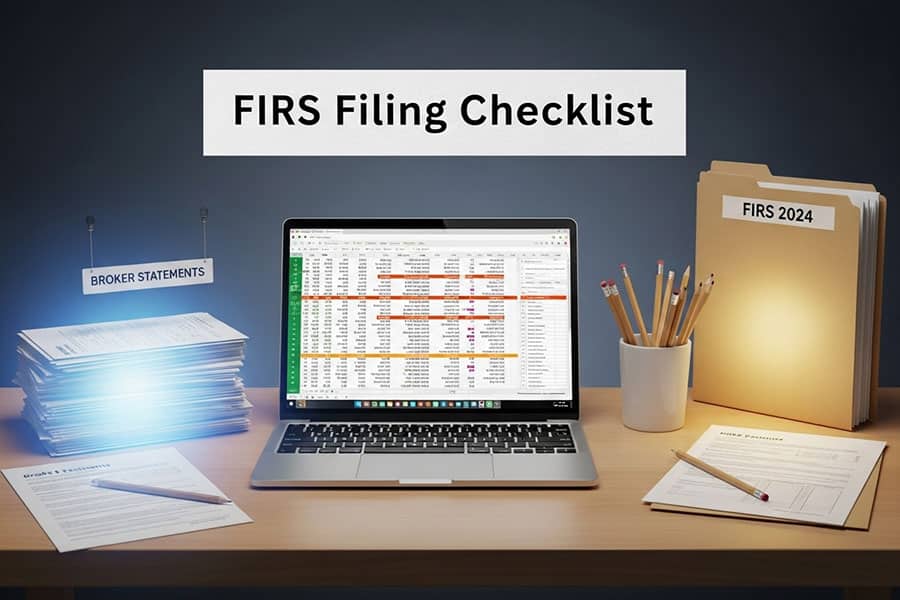

FIRS Filing Checklist

Filing your taxes can feel daunting, but with a systematic approach, it becomes a manageable annual task. I’ve developed a checklist over the years to streamline the process and ensure I don’t miss anything. This is about being organized and proactive, not reactive. Having your documents in order is the cornerstone of stress-free Nigeria tax compliance. The FIRS appreciates well-organized records, and it’s your best defense in case of an audit.

This checklist breaks down the process into three key areas: records, deadlines, and forms. Following it diligently will help you navigate the FIRS forex trading guidelines implicitly, as it forces you to gather exactly what the tax authority expects to see.

Essential Record-Keeping for Traders

- Broker Statements: Download monthly and annual statements from your forex broker. These are your primary evidence. They should show every trade, its opening and closing price, and the resulting profit or loss.

- Transaction Records: Keep a log of all deposits to and withdrawals from your brokerage account. This includes bank transfer receipts or e-wallet transaction histories. This helps prove the flow of capital.

- Personal P&L Spreadsheet: I highly recommend maintaining your own spreadsheet. This allows you to consolidate data if you use multiple brokers and to track allowable expenses. Your spreadsheet should calculate your net gain for the year.

- Communication: Save any relevant emails or communications with your broker.

Key Deadlines and Forms

- Tax Year: The Nigerian tax year runs from January 1st to December 31st.

- Filing Deadline: The deadline for filing your personal income tax return, which includes your capital gains declaration, is June 30th of the following year. So, for your 2024 earnings, you must file by June 30, 2025.

- Primary Form: You will use the Personal Income Tax Return form (Form A). Capital gains are declared within a specific section of this return.

- Filing Platform: All filing is now done electronically through the FIRS TaxPro-MAX portal. Familiarize yourself with this platform before the deadline.

Smart Deductions & Offsets

One of the most overlooked areas of managing your forex tax in Nigeria is understanding what you can legally deduct. Your tax is on *net* gains, not gross profits. This means you can subtract your losses and certain direct costs from your profits before calculating the 10% tax. This is not about tax evasion; it’s about smart, legal tax planning.

From my experience, many traders leave money on the table by not claiming legitimate deductions. The key principle is that an expense must be “wholly, exclusively, and necessarily” incurred in the process of making the profit. Think of it this way: if a cost was essential for you to be able to trade and generate that gain, it might be deductible.

What Are Allowable Expenses?

While FIRS guidelines are not explicitly detailed for retail forex traders, we can apply general principles from the Capital Gains Tax Act. Allowable expenses typically include the direct costs of transaction.

- Broker Commissions and Spreads: While spreads are built into the price, explicit commissions charged by your broker for executing trades are a direct cost.

- Bank Transfer Fees: Fees charged by your bank for wiring money to or from your international broker are a direct cost of facilitating the investment. Keep those bank statements.

- Currency Conversion Charges: If you fund your account in Naira and it’s converted to USD, any fees associated with that conversion can be considered a direct cost.

It’s important to be realistic. You cannot deduct your home office rent, internet bill, or the cost of your laptop. These are considered dual-use items and are not exclusively for trading. Stick to direct, provable transaction costs.

The Power of Loss Offsetting

The most significant “deduction” is your trading losses. You can offset your total gains with your total losses within the same tax year. If you have a bad year and your losses exceed your gains, your net capital gain is zero, and you owe no tax. You cannot, however, carry forward forex trading losses to offset gains in future years under the current rules for individuals. This makes annual profit and loss calculation critical.

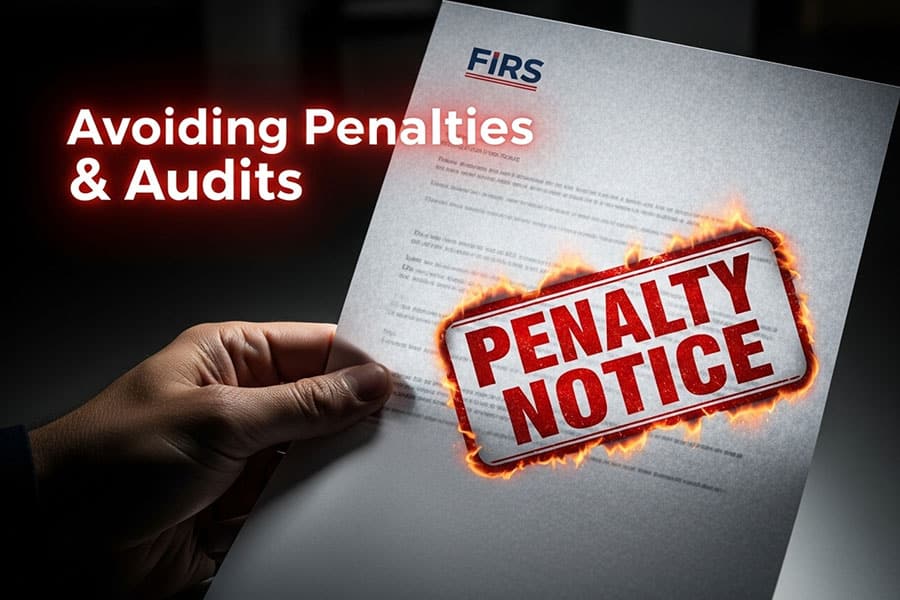

Avoiding Penalties & Audits

Nothing creates more anxiety for a trader than the thought of a letter from the FIRS. The best way to avoid penalties and audits is to build a fortress of compliance. This means being diligent, honest, and organized. The FIRS is more likely to scrutinize accounts with red flags: large, undeclared inflows of foreign currency, or a lifestyle that doesn’t match declared income.

I’ve always operated on the principle of “prepare for an audit, even if you never have one.” This mindset forces a level of discipline that not only protects you legally but also makes you a better trader. It forces you to track your performance meticulously. A core part of avoiding issues is understanding the penalty regime for non-compliance with forex tax in Nigeria.

Common Red Flags for FIRS

- Failure to File: The most obvious red flag. Not filing a tax return at all is a direct invitation for penalties.

- Under-declaration of Gains: Intentionally reporting a lower profit than what your records show is tax evasion and carries severe penalties.

- Large, Unexplained Transactions: If you are withdrawing large sums from your broker into your Nigerian bank account without declaring a corresponding capital gain, it can trigger an investigation.

- Inconsistent Records: If the numbers on your tax return don’t match the statements from your broker, it signals a problem.

Penalties for Non-Compliance

The penalties for failing to comply can be steep. They typically include:

- A fixed penalty for failure to file on time.

- Interest charged on the unpaid tax amount, calculated from the date the tax was due.

- A percentage-based penalty on the amount of tax you failed to pay.

These can add up quickly, turning a manageable tax bill into a significant financial burden. The simple act to declare forex income honestly and on time is the most effective way to avoid this.

Case Study: ₦5 M Profit

Let’s move from theory to practice. A case study is the best way to see how the principles of forex tax in Nigeria apply in the real world. Many traders struggle to connect the dots between their trading platform’s P&L and the final number they need to pay to the FIRS. Let’s walk through a realistic scenario.

Calculating Tax on a ₦5 Million Gross Profit

Meet Ade, a disciplined forex trader in Lagos. Throughout the 2024 tax year, he had a good run. Here’s a breakdown of his trading activity:

- Total Profits from Winning Trades: ₦5,000,000

- Total Losses from Losing Trades: ₦1,500,000

- Bank Wire Fees (for deposits/withdrawals): ₦50,000

- Broker Commissions (ECN account): ₦150,000

Step 1: Calculate the Net Capital Gain

We start with the gross profit and subtract the losses and allowable expenses.

Net Gain = (Total Profits) – (Total Losses) – (Allowable Expenses)

Allowable Expenses = Bank Fees + Broker Commissions = ₦50,000 + ₦150,000 = ₦200,000

Net Gain = ₦5,000,000 – ₦1,500,000 – ₦200,000

Net Capital Gain = ₦3,300,000

Step 2: Calculate the Tax Liability

Now we apply the 10% Capital Gains Tax rate to the net gain.

Tax Owed = Net Capital Gain x 10%

Tax Owed = ₦3,300,000 x 0.10

Total Tax to Pay to FIRS = ₦330,000

This example clearly shows the importance of tracking both losses and expenses. If Ade had wrongly calculated his tax on the gross profit of ₦5M, he would have overpaid by ₦170,000. This is the practical application of understanding the capital gains tax on forex profits.

Expert Tips to Minimise Liability

Beyond the basic calculations, there are several strategies and habits that I’ve seen successful, tax-compliant traders adopt. These tips are about working smarter, not harder, and positioning yourself for long-term financial health. Minimizing your liability is not about finding illegal loopholes; it’s about being diligent, strategic, and informed about the nuances of forex tax in Nigeria.

“The biggest mistake Nigerian forex traders make is treating their trading as a hobby. Once you start making consistent profits, you are running a business, and you need to adopt a business mindset. That means meticulous record-keeping and proactive tax planning. Don’t wait for FIRS to find you; file your returns voluntarily and accurately. It’s the foundation of a sustainable trading career.”

– Fictional quote by ‘Chioma Okoro, a Lagos-based Tax Consultant’

Strategic Record-Keeping

Go beyond the basics. Use a dedicated spreadsheet to log every trade. Note the date, currency pair, position size, entry/exit prices, and the P&L in both USD and NGN (using the closing day’s rate). This granular detail makes compiling your annual return effortless and provides irrefutable evidence if you’re ever questioned. This level of detail is a hallmark of professional record-keeping for traders.

End-of-Year Tax Planning

Don’t wait until June to think about your taxes. In December, review your year-to-date performance. If you have significant unrealized profits, you might consider closing some positions to lock in those gains. Conversely, if you are holding losing positions, you might close them to realize the loss, which can then be used to offset your gains for the year. This is known as “tax-loss harvesting.”

Separate Your Trading Capital

From a financial hygiene perspective, I strongly advise having a separate bank account dedicated solely to your trading activities. All deposits to your broker should come from this account, and all withdrawals should go into it. This creates a clean, easily auditable trail for your trading funds, making it much simpler to distinguish your trading capital from your personal expenses. It makes proving your case to the FIRS much easier.

Looking for a Cutting-Edge Trading Experience?

Navigating the complexities of the forex market requires a reliable partner. Opofinance, a broker regulated by ASIC, offers the tools and security serious traders need.

- Advanced Trading Platforms: Choose from MT4, MT5, cTrader, and the proprietary OpoTrade platform.

- Innovative AI Tools: Gain an edge with an AI Market Analyzer, AI Coach, and instant AI Support.

- Flexible Trading Styles: Explore opportunities with Social Trading and Prop Trading.

- Secure & Flexible Transactions: Enjoy safe and convenient deposits and withdrawals, including crypto payments with zero fees.

Conclusion

Navigating the world of forex tax in Nigeria doesn’t have to be intimidating. The core principles are clear: your profits are subject to a 10% Capital Gains Tax, meticulous records are your best friend, and proactive filing is non-negotiable. By embracing transparency and treating your trading with professionalism, you not only ensure Nigeria tax compliance but also build a more sustainable and stress-free career. The regulatory environment is evolving, making it more important than ever to stay informed and manage your obligations correctly.

Final Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial or legal advice. The author is a trader sharing experience and is not a certified tax professional. All traders should consult with a qualified Nigerian tax advisor to ensure they meet their individual compliance obligations based on their specific situation. Tax laws can and do change.

Is forex income taxable in Nigeria?

Yes, absolutely. Profits realized from forex trading are considered capital gains and are subject to a 10% tax rate by the FIRS.

What is the capital gains tax rate on forex?

The capital gains tax rate on forex profits in Nigeria is a flat 10% on your net annual gains (total profits minus total losses and allowable expenses).

How does FIRS track offshore accounts?

FIRS uses various methods, including Bank Verification Number (BVN) data, Common Reporting Standard (CRS) for automatic exchange of financial information between countries, and analysis of large transactions flowing into domestic bank accounts from abroad.

Do I pay tax if I make a loss in forex?

No. If your total losses for the tax year equal or exceed your total profits, your net capital gain is zero or negative. Therefore, you do not owe any Capital Gains Tax for that year.

Can I pay my forex tax in installments?

Capital Gains Tax is generally due as a lump sum upon filing. However, you should consult directly with the FIRS or a tax professional to see if any specific arrangements can be made in your unique circumstances.